Does My Health Insurance Cover International Travel? [FAQ]

If you’re planning an international vacation, you might be wondering what type of coverage your current health insurance plan (or Medicare) covers while you’re abroad.

In general, coverage is severely limited in these scenarios, but of course, the actual answer is more nuanced than that.

In this blog post, we’re going to field some of the most frequently asked questions surrounding health coverage while traveling abroad in a question-and-answer format. Additionally, we’ll provide some tips on where to look for coverage, how to supplement health insurance with travel insurance and travel assistance, and general best practices to make sure you have adequate coverage for your trip.

Let’s get started!

Does health insurance cover health services while abroad?

Most standard health insurance policies, including those provided by employers in the United States, offer limited or no coverage for health services received outside the country. It’s important to check your policy’s details, as some may cover emergencies but not routine care.

Does Medicare cover health services while abroad?

Healthcare coverage while traveling outside the U.S. generally isn’t included in standard Medicare plans, but there are a few exceptions.

For instance, if you’re traveling to Alaska via Canada and encounter a medical emergency, with the nearest hospital being in Canada, Medicare might cover your treatment. Additionally, there’s an option to purchase a Medigap policy, which can provide coverage for emergency medical care during international travels. Some of these plans cover medical emergency care with a lifetime cap of $50,000.

Furthermore, according to Medicare.gov, certain plans may offer coverage for emergency medical care abroad if the emergency occurs within the first 60 days of your trip and if the care isn’t already covered by Medicare. These plans might cover 80% of the billed charges for necessary emergency care outside the U.S., post a $250 annual deductible. You’ll want to contact your Medicare provider to understand the exact details of your coverage.

What’s not covered by health plans when you travel internationally?

When traveling internationally, several types of healthcare services and situations are typically not covered by standard health insurance plans, including many U.S.-based health plans:

Routine healthcare: Regular check-ups and preventive care are often not covered.

Non-emergency treatment: Treatment for non-urgent conditions or elective procedures is usually not included.

Extended care and rehabilitation: Long-term care, such as extended rehabilitation services or ongoing treatment for chronic conditions, may not be covered.

Travel vaccinations and pre-trip consultations: Pre-trip vaccinations and health consultations are often not included in standard health plans.

Repatriation or medical evacuation: The cost of medical evacuation or repatriation, if you need to be transported to your home country for treatment, is typically not covered unless you have a specific travel health insurance or a rider that includes these services.

Pre-existing conditions: An insurance provider may not cover pre-existing medical conditions while traveling abroad.

Mental health services: Coverage for mental health services, including counseling or psychiatric care, is often limited or excluded.

Dental and vision care: Routine dental and vision care are often excluded from coverage.

Prescription medications: Some plans might not cover prescriptions filled abroad or may have limitations on coverage.

Private medical facility or specialist fees: Additional fees for private hospital stays or specialist services may not be covered.

If you suspect you may need any of these services while traveling abroad, you might consider looking into a travel assistance membership from Emergency Assistance Plus.

Should I supplement my health insurance with travel insurance?

This decision largely depends on two factors: Your pre-existing conditions and the monetary value of your trip. If you know you have a condition that will likely cause you to visit a foreign hospital or receive medical treatment while abroad, you’re likely going to want to invest in a travel insurance policy that covers your needs.

Additionally, if your trip abroad is expensive, travel insurance policies can help you mitigate your losses via trip cancellation or trip interruption insurance.

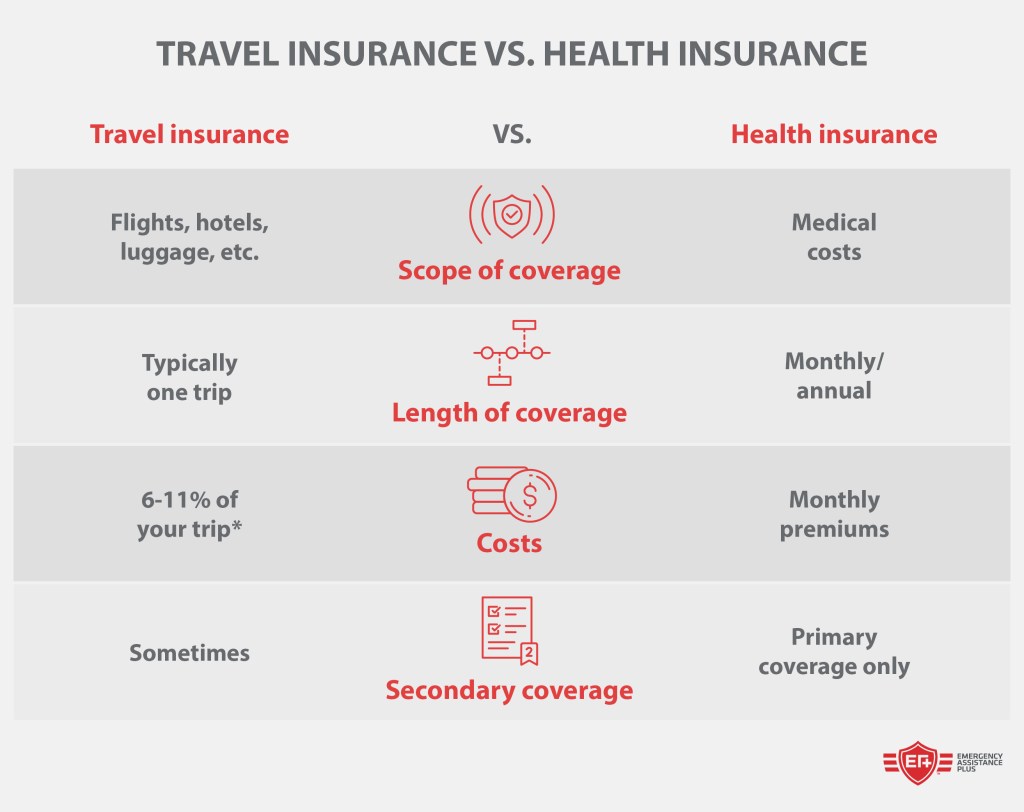

How does travel insurance differ from my health insurance?

Travel insurance guards against unexpected incidents and disruptions during travel, offering coverage for events like trip cancellations, lost luggage, flight delays, and emergency medical costs. It reimburses you for covered disruptions during your trip.

Health insurance, however, focuses on medical expenses related to illnesses, injuries, treatments, and includes hospital stays and prescriptions, offering financial support for healthcare.

Travel insurance is usually bought for specific trips with set coverage duration, including options for annual or multi-trip policies. Health insurance provides ongoing coverage, including outside travel, but often doesn’t cover international medical expenses.

The cost of travel insurance varies based on trip cost, travel duration, coverage chosen, destination risks, age, and health. Expect to pay around 6-11% of your trip’s value, considering factors like co-pays and deductibles. Health insurance premiums depend on age, health history, coverage level, and plan type (like HMO or PPO).

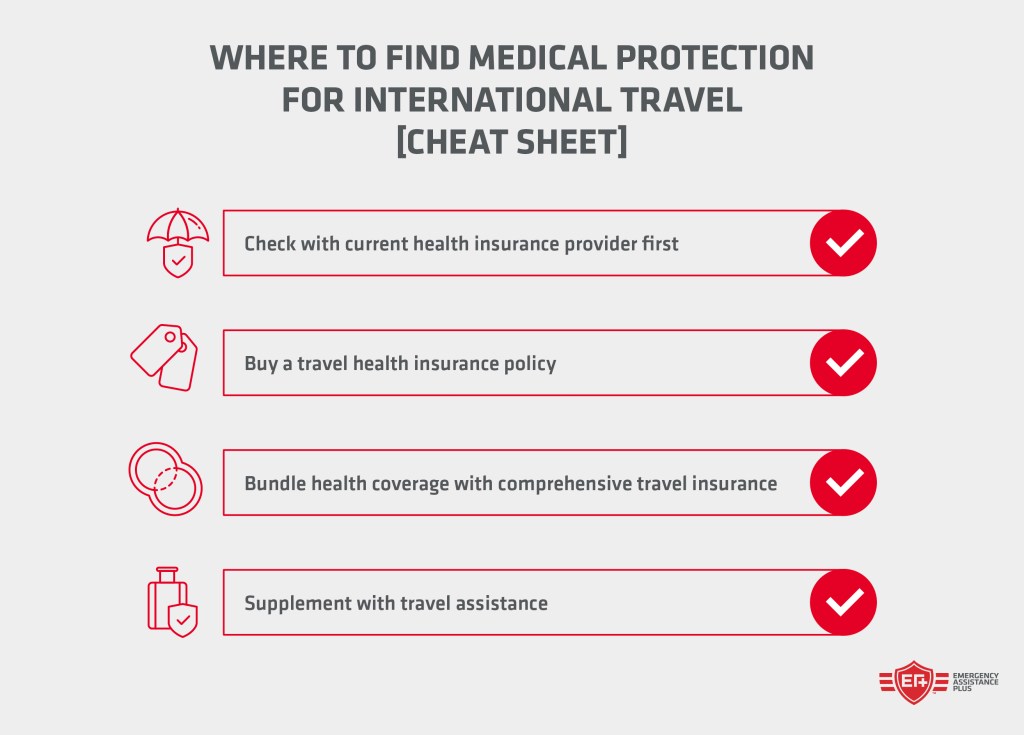

How can I get medical coverage for international travel?

You have a few different options for medical insurance and other services for international coverage.

Check existing health insurer: First, review your current health insurance coverage to understand what, if any, medical coverage it offers for international travel. Some policies may include limited coverage for emergencies abroad.

Purchase travel health insurance: If your existing health insurance doesn’t provide sufficient coverage, consider buying a travel health insurance policy. This type of insurance is specifically designed to cover medical emergencies, hospitalizations, and sometimes even medical evacuation while you are traveling abroad.

Consider a comprehensive travel insurance policy: Along with travel health insurance, you can opt for a comprehensive travel insurance policy that includes medical coverage as well as other protections like trip cancellation, interruption, lost luggage, and travel delays. Get a free travel insurance quote with TripInsure Plus, available exclusively to current EA+ members!

Enroll in a travel assistance membership: Unlike travel insurance, travel assistance can reimburse you for financial loss and actually provide services if you have an emergency medical situation. Examples include ambulance services, emergency medical evacuation, and other emergencies that require medical attention. See more details about protection from EA+ here.

Where should I buy travel insurance?

There are several different channels where you can buy travel insurance, each with its own advantages. Here are some common places where you can buy travel insurance:

Travel Insurance Companies: Buying directly from a specialized travel insurance company is often the best way to get comprehensive coverage. These companies offer a range of plans and options tailored to different types of travel needs. You can compare policies and prices online on their websites. Tripinsure Plus is a great complement to travel assistance from EA+. Get a free quote here.

Travel Agencies and Tour Operators: When booking a trip, travel agencies and tour operators often offer travel insurance as an add-on. This can be convenient, but it’s important to ensure that the coverage meets your specific needs.

Insurance Brokers or Agents: An insurance broker or agent can help you navigate the various options and find a policy that best suits your travel plans and coverage needs. They can provide personalized advice and explain the finer details of different policies.

Credit Card Companies: Some credit cards offer travel insurance as a benefit for cardholders, particularly premium or travel-oriented credit cards. However, the coverage provided is often limited and may not be sufficient for your needs, so it’s important to read the terms carefully.

Online Comparison Websites: There are numerous websites where you can compare travel insurance policies from different providers. These platforms allow you to enter your travel details and compare plans based on price, coverage, and other factors.

Membership Organizations: If you are a member of certain organizations or clubs (like AAA or AARP), you might have access to group travel insurance rates or policies tailored to members.

No matter where you purchase, do your research to ensure that:

The provider is reputable and has good customer reviews

You’ve compared different policies to find one that fits your specific needs and budget

You’ve read the fine print carefully to understand what is and isn’t covered.

You’ve checked for any exclusions, especially if you have pre-existing medical conditions or plan to engage in high-risk activities.

How to file a claim for medical care that was outside the U.S.

Depending on if you’re filing a claim for medical services with your health insurance plan, your travel insurance company, or somewhere else, the process might vary. However, regardless of where you file the claim, here are a few universal best practices:

Gather documentation: Collect all relevant documents related to the medical care you received. This includes detailed medical bills, receipts, diagnosis reports, treatment details, and discharge summaries. If the documents are not in English, you might need to get them translated.

Contact your insurance company: As soon as possible, inform your insurance company about the medical care you received. They will guide you on their specific claim process and inform you of any additional documentation needed.

Claim forms: Your insurer will likely require you to fill out a claim form. Complete this form accurately, providing detailed information about the medical services received and the reason for treatment. Make sure to include your policy number and other necessary identification details.

Submit claims promptly: There is often a time limit for submitting claims (e.g., within 90 days of receiving treatment). Submit your completed claim form along with all required documents within this time frame.

Keep copies: Make copies of all documents and forms you submit for your own records. This will be useful if there are any questions or issues with your claim.

Direct payment or reimbursement: Depending on your policy, the insurer might pay the medical provider directly, or you may need to pay upfront and seek reimbursement. If you paid for the medical expenses, include proof of payment with your claim.

Follow up: After submitting your claim, follow up with your insurance company to check the status. Be prepared for additional requests for information or clarification.

Appeal if necessary: If your claim is denied or you disagree with the decision, you have the right to appeal. Your insurer will provide instructions on how to do this.

Next steps

Now that you know the limits of most health insurance plans when it comes to international travel, you may want to supplement your coverage.

For travel insurance, consider getting a free quote from TripInsure Plus. With affordable rates and best-in-class coverage, it’s a great way to protect the investment of your trip. Note: TripInsure Plus is available exclusively to current EA+ members.

So when you supplement your travel insurance plan with travel assistance from EA+, EA+ members carry the assurance that, no matter if they are on a exotic vacation or just a short drive from their house, a team of expert professionals is always prepared to respond in the event of a medical emergency. This team ensures members receive the appropriate medical treatment and arranges the needed transportation back home, providing peace of mind during their travels.

About the Author

Bryanna Moore, Senior Product Manager

Bryanna has been with Emergency Assistance Plus (EA+) for nearly 20 years, starting in customer service and now, as Senior Product Manager, she is responsible for member experience – including ensuring that the services EA+ provides continues to meet the evolving needs of EA+ members. Bryanna is passionate about EA+ members and making sure that Emergency Assistance Plus delivers on its brand promise to get members home safely in their time of need.

Stay in the Know

If knowledge is power, you’ll be at your strongest by subscribing to our newsletter, which will keep you informed of the latest updates and improvements to the EA+ programs, not to mention travel tips and member stories.

This website uses cookies to enhance user experience and to analyze performance and traffic on our website. We also share information about your use of our site with our social media, advertising and analytics partners. Privacy Policy

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

This website uses cookies to enhance user experience and to analyze performance and traffic on our website. We also share information about your use of our site with our social media, advertising and analytics partners. Privacy Policy

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.